An Aging Workforce and Your Workers’ Comp: The Costs Are Not What You Think

As the workforce ages, many employers worry about rising workers’ compensation costs. The assumption is that older employees are more expensive to insure. However, national data tells a different story.

For businesses concerned about their bottom line, an experienced workforce does not automatically mean higher claim costs. In many cases, the opposite is true.

Lower Wages Drive Down Claim Costs

A report from the National Council on Compensation Insurance (NCCI) reveals a key trend: while an employee’s wages typically peak around age 50, they often decline significantly after age 65. This is commonly due to employees shifting to part-time schedules or different roles.

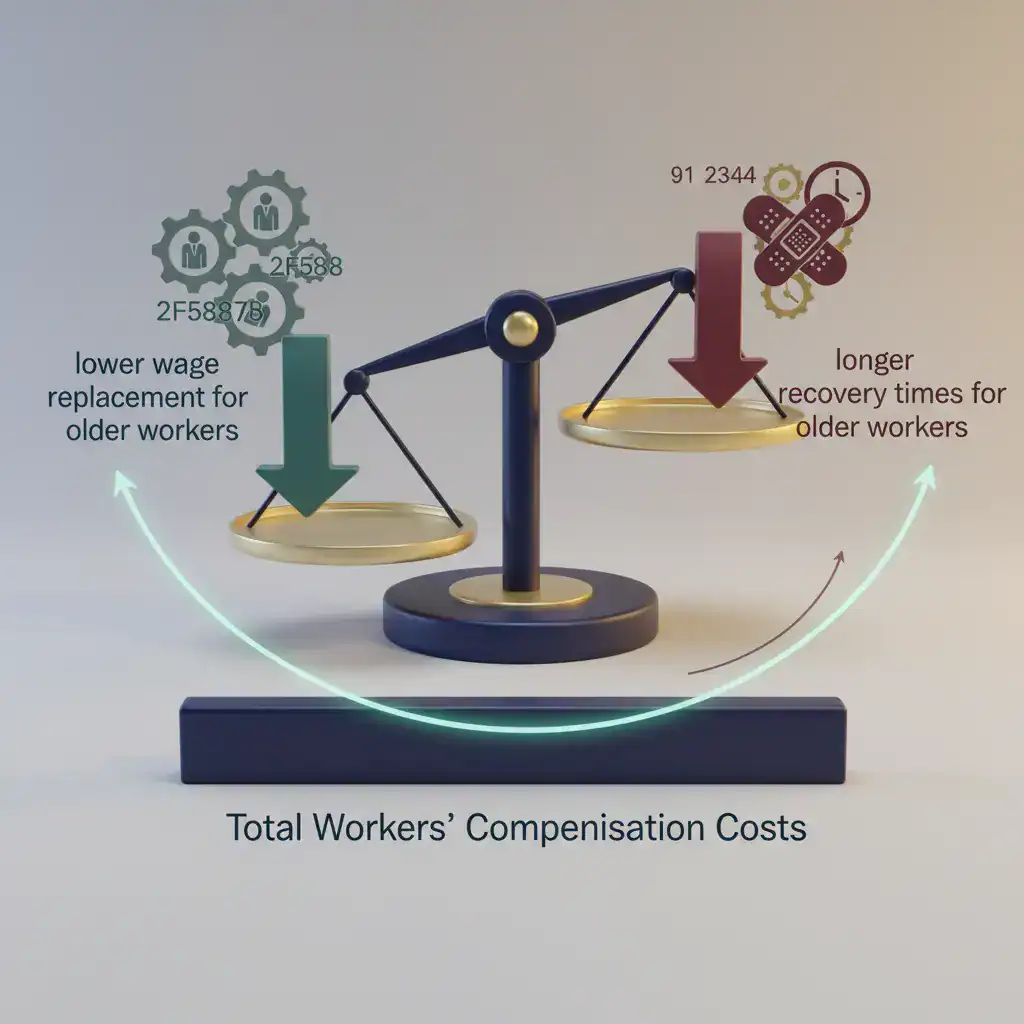

This wage decrease has a direct impact on the cost of a workers’ comp claim.

A major portion of a claim’s cost is “indemnity” — the wage replacement paid to an employee while they recover. Because these payments are calculated as a percentage of the employee’s current wage, a lower wage translates directly to a lower payment from the insurer.

The result is a substantial cost reduction. The NCCI found that the average cost of lost-wage payments for workers 65 and older is roughly 20% lower than for workers in the 60-64 age group.

But Don’t Older Workers Take Longer to Heal?

Yes. Data confirms that recovery times are longer for older workers. The median time away from work for an injured employee over 65 is 16 days, compared to just 10 days for those aged 45-54.

While a longer recovery period seems like it would increase costs, this effect is more than offset by the lower wage base. The smaller weekly payment, even when stretched over a slightly longer period, typically results in a lower total payout for the claim.

Industry Matters: Key Exceptions to the Rule

This trend does not apply universally. The risk profile for older workers changes depending on the industry.

- Higher-Risk Industries: The leisure, hospitality, and retail sectors often see higher than average claim costs for older workers. These environments have a high frequency of slips, trips, and falls — the leading cause of injury for this age group.

- Lower-Risk Industries: Conversely, in historically hazardous fields like manufacturing and construction, older workers tend to file fewer claims. This is often attributed to their deep experience, safety consciousness, and reliability.

The Bottom Line for Employers

Fears that an aging workforce will automatically inflate your workers’ compensation costs are largely unfounded.

The data is clear: older employees are often safer, more reliable, and, from a wage-replacement perspective, less costly to insure when an injury occurs. A robust safety program that protects all employees is your best strategy. An experienced, multi-generational workforce is a powerful asset, not a workers’ comp liability.

The Technical Edge

The indemnity cost reduction for older workers is a function of state workers’ comp wage replacement formulas. In most states, temporary total disability (TTD) is paid at 66.67% of the employee’s pre-injury average weekly wage (AWW), subject to a state maximum. A part-time retail worker over 65 earning $400/week receives $267/week in TTD. A full-time manufacturing worker aged 35 earning $900/week receives $600/week. The same 16-day recovery that costs $1,371 in TTD for the older worker costs $3,086 for the younger worker — a 125% difference driven entirely by the wage base, not the injury.

The 16-vs-10-day median recovery comparison in the “Longer to Heal” section understates the actual financial impact because it does not account for the interaction with state waiting periods: most states have a 3-7 day waiting period before TTD begins. For a 10-day absence, the waiting period absorbs 30-70% of the total disability period, meaning many younger workers’ injuries fall entirely within the waiting period and generate zero indemnity. For the 16-day older worker absence, the same waiting period absorbs a smaller fraction of the total absence. The industry exception for leisure/hospitality/retail is consistent with BLS data on fall injury rates by age and industry: slip-and-fall injuries increase in frequency with age across all industries, but the severity increase is largest in retail and food service because these environments have higher floor-level hazard exposure and less structured PPE or safety culture than manufacturing.

The ADEA (Age Discrimination in Employment Act) implication for employers: workers’ comp management decisions that disproportionately affect employees over 40 can create ADEA exposure. Specifically, an employer who terminates older employees on workers’ comp at higher rates than younger employees in similar situations faces a pattern discrimination risk. The data in this post cuts the other way — treating older workers as an insurance liability is factually incorrect and legally risky.

The 14-Point Workers’ Comp Annual Checkup at WorkCompProfessionals.com includes the workforce demographic review that helps employers understand how age distribution is actually affecting claim frequency and cost — vs. how they assume it is.

Agents who want to help employers understand the real cost dynamics of an aging workforce will find tools and training at WorkCompProfessionals.com. Employers who want to build safety and claims management strategies tailored to a multi-generational workforce can find practical guidance at ConquerCompCosts.com.