The Georgia Contractor Trap: The Statutory Employer

Quick Takeaways

- The Trap: In Georgia, if you hire a sub without insurance, you are their workers’ comp carrier. Your contract won’t save you from the medical bills.

- The Rule: Georgia Code § 34-9-8 states that a principal is liable for workers’ comp benefits to employees of an uninsured subcontractor.

- The Fix: Verify every sub’s COI with the carrier directly. If they miss a payment, you become the statutory employer.

- Learn More: Agents can see how IWCP membership keeps you ahead. Employers can take control at LockedAndLoadedTraining.com.

Are you sure your subs are covered?

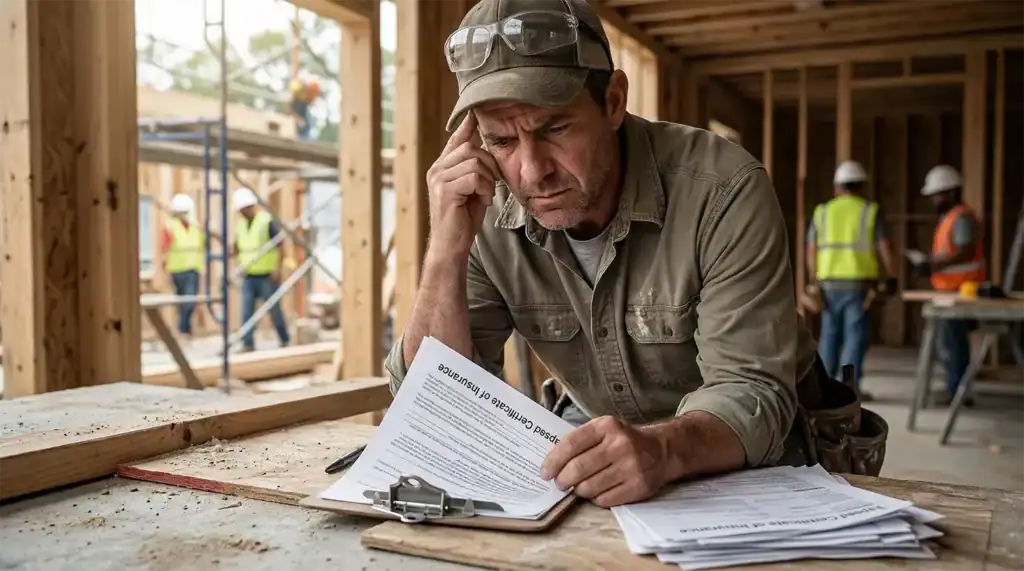

You hire a crew for a framing job in Atlanta. They hand you a certificate of insurance (COI), sign your “independent contractor” agreement, and get to work. You think you’ve managed your risk. You think you’ve shifted the liability.

Think again. You might have just walked into a trap.

In Georgia, the law makes sure someone pays when there’s a broken arm. If your subcontractor’s policy lapses, your “hold harmless” clause won’t matter. The state will look up the chain, and that person is you. You become the Statutory Employer, meaning you pay for the injury now and higher premiums for the next three years.

The Statutory Employer in Georgia

The world of Georgia workers’ comp is full of missing, outdated, or inaccurate COI’s.. Many contractors mistakenly think a piece of paper in the file keeps them safe. Don’t let standard industry inertia put your business at risk. Under Georgia law, your liability is active as long as the worker is on your job site.

Why your contract doesn’t override the statute

Want to spend thousands on lawyers to draft airtight subcontracts? Go ahead. But you can’t contract away your statutory obligations. If a subcontractor is uninsured at the moment of injury, the law treats them as your employee for workers’ compensation.

This is a common mistake when hiring subcontractors. Many employers think a signed piece of paper protects them. But the Commission deals in facts. No policy equals liability for you.

The COI is just a snapshot

Suppose a sub hands you a COI showing workers’ comp coverage. You file it away. Two months later, they miss a premium payment, and the carrier cancels the policy. They don’t tell you. You don’t ask.

Then the accident happens.

That COI is now worthless. There is no perfect solution, but collecting a new COI every time you hire the same contractor for a new job is a great start. Their insurance company may be required to notify you if the policy is cancelled, but that notice won’t be delivered for 30-45 days after the cancellation. Not knowing is not a defense, the system protects the injured worker first.

Fortune Favors the Boldly Vigilant

Build a structured process to collect and organize the certificates of insurance from your subcontractors. Get a new certificate each time you hire the same sub for a new job. If the contractor is working on a long term job, make a plan to request a new certificate or otherwise verify their coverage is active periodically.

Don’t let your profit margin disappear due to someone else’s negligence.

Master the rules and take control of your process. Agents can learn the protocols at the Institute. Employers can take control of their costs at LockedAndLoadedTraining.com.

Fortune favors the bold, but it really favors the one who takes action.