|

||

| |

|

|

Sixteen warning signals that your insurance company may have overcharged you on your Workers' Compensation Premium Audit

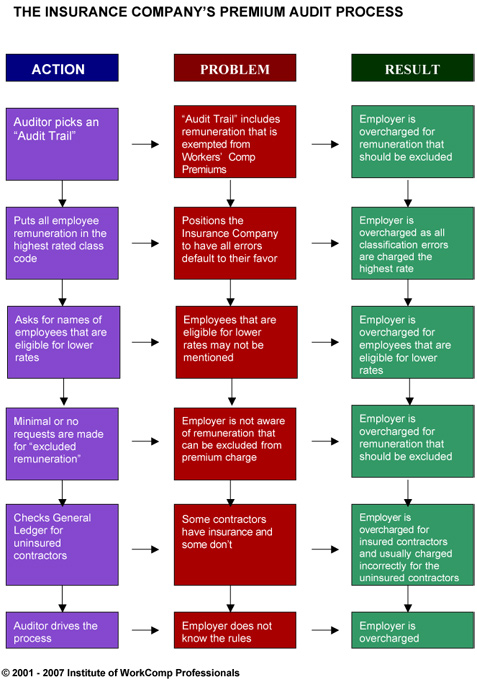

Unlike IRS audits, most businesses consider the Workers' Compensation Premium Audit a routine business requirement that is conducted annually to ensure compliance with state laws. Regularly, a bookkeeper or administrative assistant with little understanding of Workers' Compensation is asked to get the auditor what he or she needs. Invariably, it is assumed that the audit will be done properly and any findings will be correct.

Yet, with over 600 types of classifications, complex rules regarding excluded remuneration, executive payroll, and subcontractors, mistakes are common. It is very easy, and not unusual, for employers to unknowingly leave money on the table.

Auditors have demanding schedules and most do not have the time, or inclination, to educate clients. The process is set up so that all payroll is assigned to the highest rated code, thus ensuring that any mistakes default to the advantage of the insurance company.

How do you know if you have been overcharged? Here are 16 warning signals that should trigger additional scrutiny:

| 1 | You did not get a copy of the auditor's worksheets. |

| 2 | The audit was conducted at the accountant's or bookkeeper's office. The term, “audit” often is synonymous with accountant, although many accountants have little, if any knowledge of the laws governing Workers' Compensation. |

| 3 | The insurance company changed your basic classification or reallocated payroll. |

| 4 | Your Experience Mod increased during the policy period. |

| 5 | Charges were made for uninsured subcontractors or owner-operators. A common error is that payroll is charged on the contract price, not actual payroll. |

| 6 | The audit included a charge for paid commissions. |

| 7 | You received a large additional or return premium (you may be entitled to more). |

| 8 | The state implemented a rate change. | 9 | Credits on last year's policy were removed from your current policy. |

| 10 | You are a contractor involved in several types of work, but not all of them are shown on your policy. |

| 11 | Your policy was cancelled or rewritten with a different effective date. |

| 12 | The wages of an executive officer of the corporation were assigned to high-rated classifications. |

| 13 | You are a contractor involved in a wrap-up construction project. |

| 14 | Your policy contains a Residual Market or Assigned Risk surcharge. |

| 15 | You were awarded contracts under the Davis-Bacon Act. |

| 16 | You are not absolutely certain that you didn't overpay your audit. |